What the Latest Central Bank Decisions Mean for Investors and Gold

The world's biggest central banks have spoken, but how do their latest interest rate decisions affect you? From savings and mortgages to bonds, shares, and gold, here's how recent policy changes could affect your investments and what to look out for next.

June has been another important month for investors, with the Federal Reserve, European Central Bank, Bank of England, and Swiss National Bank all delivering fresh policy decisions.

Interest rates may sound like something only economists worry about, but central bank decisions influence almost every part of the financial system. They affect mortgage costs, savings accounts, bond prices, stock markets and even the price of gold.

Understanding what central bank interest rates mean can help investors make more informed decisions and avoid being overwhelmed by financial headlines.

What Happened?

Federal Reserve (17 June 2026)

The Federal Reserve left interest rates unchanged, signalling that policymakers remain cautious about cutting rates further until they are confident inflation is moving sustainably towards target.

European Central Bank (11 June 2026)

The ECB maintained a cautious approach as inflationary pressures remain a concern in parts of the euro area.

Bank of England (18 June 2026)

The Bank of England held rates steady as policymakers continue to balance slowing economic growth against inflation that remains above its long-term target.

Swiss National Bank (18 June 2026)

The SNB maintained its policy rate at 0%, reflecting Switzerland's relatively subdued inflation environment.

Why Are Central Banks Acting Now?

Central banks are primarily trying to achieve two objectives:

- Keep inflation under control.

- Support sustainable economic growth.

The challenge is that these goals often pull in opposite directions. Higher interest rates help reduce inflation but can slow economic activity. Lower rates support growth but can risk reigniting inflation.

This balancing act helps explain why central banks have become increasingly cautious after several years of economic shocks.

How Inflation And Interest Rates Have Interacted

Why Have Interest Rates Changed So Much?

The sharp rise in inflation after the COVID-19 pandemic was initially driven by supply chain disruptions and strong consumer demand as economies reopened. Shortages pushed up the price of everything from cars to electronics.

Russia's invasion of Ukraine in early 2022 added a further inflationary shock. Higher energy and food prices pushed inflation to levels not seen for decades.

In response, central banks embarked on one of the most aggressive interest-rate hiking cycles in modern history. By making borrowing more expensive, policymakers aimed to slow spending and bring inflation back under control.

As supply chains recovered and inflation began to ease during 2023 and 2024, central banks were able to slow and eventually reverse some of those increases.

However, progress has not been entirely smooth. New trade tariffs introduced in 2025 increased concerns about rising costs, while conflict involving Iran and renewed tensions in the Middle East in 2026 caused oil prices to spike, threatening fresh inflationary pressures.

These developments help explain why central banks have become more cautious about cutting rates further. While inflation has fallen significantly from its post-pandemic highs, policymakers remain wary that price pressures could prove more persistent than expected.

What Does This Mean For Cash Savings?

Higher interest rates generally benefit savers.

Banks tend to offer more attractive savings rates when central bank rates are high, although savings rates do not always move in lockstep with policy rates.

The key consideration is the difference between savings rates and inflation. A savings account paying 3% may look attractive, but if inflation is running at 4%, purchasing power is still falling.

What Does This Mean For Bonds?

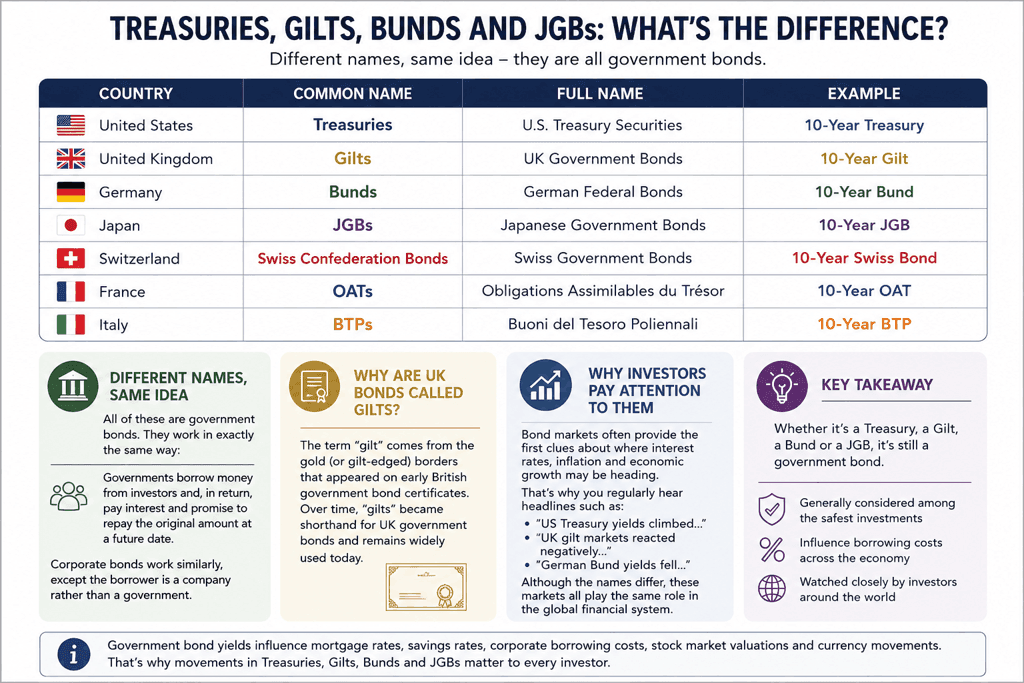

Bonds are essentially loans. When governments or companies need to raise money, they can issue bonds, promising to repay investors on a set date while paying interest along the way.

Government bonds are issued by national governments and are generally considered among the safest investments available, as a result their yields influence borrowing costs and investment returns throughout the wider economy.

Different countries use different names for their government bonds:

Despite their different names, they all serve the same purpose: allowing governments to borrow money from investors.

Companies can also issue bonds, known simply as corporate bonds, which generally offer higher yields to compensate investors for taking on greater risk.

Why Bond Prices Move Opposite To Interest Rates

Bond prices and interest rates typically move in opposite directions.

When interest rates rise, newly issued bonds offer higher yields. Existing bonds with lower coupon payments become less attractive, causing their prices to fall.

Conversely, when interest rates decline, existing bonds often rise in value.

For example, imagine you own a UK gilt paying 2% interest. If newly issued gilts begin offering 4%, investors are unlikely to pay full price for your lower-yielding bond. Its market value will fall until its effective yield becomes competitive with newer bonds.

This relationship explains why many bond markets struggled during the global tightening cycle of recent years.

Why Bond Markets Matter To Everyone

Even investors who never buy bonds are affected by them.

Government bond yields influence:

- Mortgage rates

- Savings rates

- Corporate borrowing costs

- Stock market valuations

- Currency movements

This is why financial markets pay such close attention to movements in:

- US Treasuries

- UK Gilts

- German Bunds

- Japanese Government Bonds (JGBs)

These markets often react to inflation and interest-rate expectations before other asset classes, making them an important indicator of where investors believe the economy is heading.

What Does This Mean For Equities?

Higher interest rates can create challenges for stock markets.

Companies face higher borrowing costs, while future profits become less valuable when discounted at higher interest rates.

This tends to affect high-growth companies most strongly.

However, the relationship is not always negative. If rates remain relatively high because economic growth is healthy and company earnings are rising, equities can continue to perform well.

What Does This Mean For Gold?

The relationship between interest rates and gold is often misunderstood. Many investors assume higher interest rates automatically lead to lower gold prices but the reality is more nuanced than that.

Gold does not generate income, so higher interest rates can increase the opportunity cost of holding it. However, investors tend to focus on real interest rates - nominal interest rates after inflation has been taken into account.

If inflation remains elevated, real returns on cash and bonds may still be relatively low, even when headline interest rates appear attractive.

Gold is also influenced by factors beyond interest rates, including:

- Inflation concerns

- Currency weakness

- Geopolitical tensions

- Financial market volatility

- Concerns about government debt

This helps explain why gold can sometimes perform well even during periods of relatively high interest rates.

What Investors Should Watch Next

Several factors are likely to influence central bank decisions during the remainder of 2026:

Inflation Data

Inflation remains the single most important driver of monetary policy.

Labour Markets

Employment and wage growth provide clues about future inflationary pressures.

Energy Prices

Oil and gas prices remain particularly sensitive to geopolitical developments.

Central Bank Guidance

Markets often react more strongly to policymakers' comments about future decisions than to the rate decision itself.

Geopolitical Risks

Trade tensions, tariffs, and conflicts in key energy-producing regions continue to influence inflation expectations and investor sentiment. Changes in political leadership - particularly when accompanied by a significantly different economic strategy - can also impact markets.

The Bottom Line

Central bank decisions influence far more than borrowing costs.

Through their impact on savings, bonds, equities and gold, interest rates shape the investment environment that all investors operate within.

Trying to predict every policy move is difficult. For most investors, maintaining a long-term perspective and holding a diversified portfolio remains more important than reacting to every headline.

Understanding why central banks make the decisions they do can help investors make more informed decisions and stay focused on their long-term financial goals.